The Trump-GOP Health Care Emergency: War on Your Health Care ResearchFact SheetNews The Trump-GOP Health Care Emergency: War on Your Health Care The fallout from Donald Trump and Republicans’ big, ugly bill is happening now, causing severe…ashoupAugust 4, 2025

FACT SHEET: Republicans’ Big Ugly Bill Will Kick Seniors Out Of Nursing Homes And Shutter Over A Quarter Of Facilities ResearchFact SheetNews FACT SHEET: Republicans’ Big Ugly Bill Will Kick Seniors Out Of Nursing Homes And Shutter Over A Quarter Of Facilities Over A Quarter Of Nursing Homes Will Be Forced To Close Under The GOP Bill…ashoupJune 27, 2025

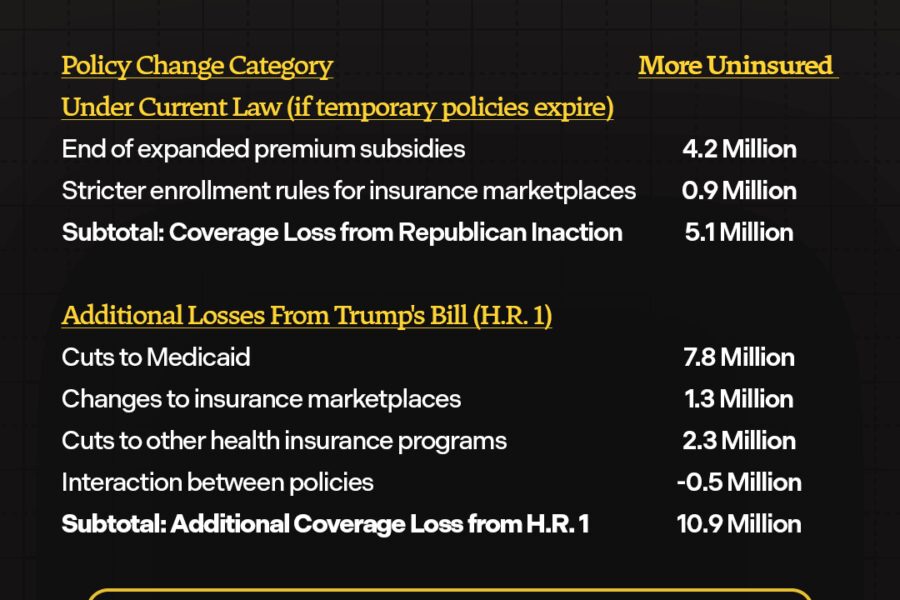

FACT SHEET: 16 Million Americans Will Lose Their Health Care Under the GOP Tax Scam ResearchFact Sheet FACT SHEET: 16 Million Americans Will Lose Their Health Care Under the GOP Tax Scam The Republican Big, Terrible Bill Is Getting Worse By the Day Republicans have supercharged their…ashoupJune 6, 2025

NEW REPORT: Medicaid Coverage Is at Risk for Millions in the Asian American, Native Hawaiian, and Pacific Islander Community ResearchReportNews NEW REPORT: Medicaid Coverage Is at Risk for Millions in the Asian American, Native Hawaiian, and Pacific Islander Community The GOP Scheme Will Raise Costs and Rip Coverage Away from AANPHI Communities Read the…ashoupMay 30, 2025

Republican Premium Hikes Will Raise Health Care Costs for Everyone ResearchFact Sheet Republican Premium Hikes Will Raise Health Care Costs for Everyone Small Business Owners, Middle Class Families, And Rural Communities Will Be Among The Hardest Hit…ashoupMarch 24, 2025

FACT SHEET: Trump’s Crusade Against The ACA Continues With Renewed Attacks On The Law In His Second Term Fact Sheet FACT SHEET: Trump’s Crusade Against The ACA Continues With Renewed Attacks On The Law In His Second Term Since its passage 15 years ago, the Affordable Care Act (ACA) has become the bedrock…ashoupMarch 19, 2025

GREED WATCH: As Trump Conspires With Drugmakers to Raise Costs on Americans, Records Show Massive 2024 Earnings ResearchNews GREED WATCH: As Trump Conspires With Drugmakers to Raise Costs on Americans, Records Show Massive 2024 Earnings Drugmakers Raked in $610 Billion in 2024, Spent $90 Billion Rewarding Shareholders, And Sued The…ashoupFebruary 20, 2025

NEW REPORT: The Republican War on Health Care: Medicaid Cuts for Millions, Tax Cuts for the Ultra-Wealthy ResearchReportNews NEW REPORT: The Republican War on Health Care: Medicaid Cuts for Millions, Tax Cuts for the Ultra-Wealthy Protect Our Care Releases New Report Detailing the Republican War on Health Care Threatening More…ashoupFebruary 11, 2025

Fact Sheet: RFK Jr. Spread Conspiracy That Lyme Disease Came From a Military Bioweapon ResearchFact SheetNews Fact Sheet: RFK Jr. Spread Conspiracy That Lyme Disease Came From a Military Bioweapon In recent weeks, Robert F. Kennedy Jr. has been on a whirlwind tour attempting to…ashoupJanuary 24, 2025

FACT SHEET: RFK Jr.’s Plans To Defund, Slash Jobs and Undermine the National Institutes of Health Would Be Disastrous For Americans NewsResearchFact Sheet FACT SHEET: RFK Jr.’s Plans To Defund, Slash Jobs and Undermine the National Institutes of Health Would Be Disastrous For Americans RFK Jr. Has Vowed to Fire and Prosecute Hundreds of NIH And FDA Employees and…ashoupJanuary 22, 2025