At 11:15 am today, President Trump will sign an Executive Order to sabotage our health care. Having failed at health care repeal in Congress because of bipartisan opposition and overwhelming public rejection, the Trump administration is now doing everything it can to sabotage the country’s health care system and fulfill his promise to “Let it be a disaster.”

Protect Our Care is releasing this new video documenting how the elements of this Executive Order already reported by the press amount to government sabotage of our health care and how previous efforts at sabotage have already brought harm to people and their coverage, and urging Members of Congress to stand up to it.

The Trump administration’s sabotage agenda could end affordable coverage for those with pre-existing conditions, raise health care premiums and deny access to coverage for millions of Americans — and could result in the destabilization of the individual insurance market.

As was just announced, California will impose an average 12.4 percent surcharge on health care premiums for the benchmark silver plan offered through Covered California because of efforts by President Trump and Republicans in Congress to sabotage our health care by threatening to withhold cost-sharing reduction payments. While they have been unable to repeal the health care law, they have been doing everything they can to sabotage the marketplace by:

Threatening to defund the law’s mandatory cost-sharing-reduction payments, which the nonpartisan Congressional Budget office said would increase rates by 20% in 2018 and 25% in 2020.

Slashing 90% of the funding to let people know when and how they can sign up for coverage.

Prohibiting Regional Directors from the Department of Health and Human Services from participating in efforts to help people enroll in coverage during open enrollment.

Shutting down HealthCare.gov during critical hours.

Cutting the number of days people can sign up for coverage in half.

On the first day of this administration, President Trump signed an Executive Order demanding that agencies dismantle as much of the law as they can.

Now people are facing the consequences.

“Everyone with the benchmark plan who gets a bill from their insurer for higher health care costs next year can thank President Trump and Republicans in Congress for the sabotage that led to this,” Protect Our Care Campaign Director Brad Woodhouse said. “Their repeated threats, uncertainty and sabotage of our health care system is taking a toll on real people’s lives in California. Your health care bills next year should say ‘brought to you by Donald Trump.’”

EXPERTS AND INSURANCE COMMISSIONERS AGREE THAT TRUMP’S SABOTAGE IS RAISING COSTS:

Center for American Progress: “The Center for American Progress estimates that uncertainty around CSRs and mandate enforcement will raise 2018 premiums for benchmark coverage an extra $1,061 annually for a 40-year-old and $2,491 annually for a 64-year-old.” [Center for American Progress, 8/16/17]

Kaiser Family Foundation: “Benchmark Premiums Would Increase By 19 Percent On Average If Cost-Sharing Subsidies Were Unpaid.” [KFF, 4/6/17]

Urban Institute: “We Find That Premiums For Silver Marketplace Plans Would Increase $1,040 Per Person On Average.” [Urban Institute, 1/16]

Urban Institute: “A Precipitous Drop In Insurer Participation Is Even More Likely If The Cost-sharing Assistance Is Discontinued.” [Urban Institute, 12/6/16]

Julie Mix Mcpeak, President-Elect Of The National Association Of Insurance Commissioners And Tennessee State Insurance Commissioner: “I Am Very Fearful That We’ll Have Insurers Make A Decision To Leave Markets As A Result Of The Uncertainty.” [New York Times, 8/7/17]

Teresa Miller, Pennsylvania Insurance Commissioner: “Failing To Make Payments To Insurers For Cost-sharing Reductions Would Force Insurers To Request A Statewide Average 20.3 Percent Increase Rather Than 8.8 Percent Statewide Average That Was Filed With The Department In May.” [Press Release, 7/31/17]

Mike Kreidler, Washington State Insurance Commissioner: “The Current Federal Administration’s Actions — Such As Not Committing To Reimburse Insurers For Cost-sharing Subsidies And Not Enforcing The Individual Mandate — Appear Focused Only On Destabilizing The Insurance Market.”[Statement, 6/19/17]

Lori Wing-Heier, Director, Alaska Division Of Insurance: “It Is Expected That Health Care Premiums Would Jump As High As 20 Percent If Trump Follows Through With His Threat To Cut Subsidies.” [Fairbanks News-Miner, 8/14/17]

Dave Jones, California State Insurance Commissioner: “President Trump Appears On A Mission To Destroy Health-Insurance Markets By Creating Instability Through His Own Actions And Thereby Depriving Millions Of Americans Of Health-care Coverage.” [Wall Street Journal, 6/27/17]

Marguerite Salazar, Colorado’s State Insurance Commissioner: “Commissioner Marguerite Salazar Said The Trump Administration Threatens The Whole Market. ‘My Fear Is It May Collapse.’” [Los Angeles Times, 5/18/17]

Craig Wright, Chief Actuary, Florida Office of Insurance Regulation: “If The Subsidies Are Not Funded, Carriers Would Face The Prospect Of Large Financial Losses.” [New York Times, 8/7/17]

Eric A. Cioppa, Superintendent Of The Maine Bureau Of Insurance: “If They Don’t Get A Subsidy, I Fully Expect Double-Digit Increases For Three Carriers On The Exchanges Here.” [New York Times, 6/4/17]

National Academy for State Health Policy: “The Federal Government Must Commit To Funding CSR Payments In Order To Lower Rates And Stabilize Carrier Participation.” [Letter from State-based Marketplace Directors, 8/30/17]

Dan Hilferty, President And CEO, Independence Blue Cross: “We Firmly Believe Your Coverage Will Be There For 2018, If The Federal Government, Congress And President Commit To, Fund The Subsidies During An Interim Period Of Time.” [CNN, 7/19/17]

Kelly Paulk, Vice President, Product Strategy And Individual Markets, Blue Cross Blue Shield Of Tennessee: “We Have To Factor In Two Significant Uncertainties…Combining Those Two Factors Leads To An Average 21 Percent Rate Increase.” [Blog Post, 6/30/17]

Danielle Devine, Michigan Director Of Operations, Meridian Health Plan: “The Political Climate Continues To Make It Difficult To Price And The Uncertainty Over The Future Of The Subsidies Creates The Largest Reason For Significant Rate Increases.” [Crain’s Detroit Business, 6/14/17]

Rick Notter, Director Of Individual Business, Blue Cross Blue Shield Of Michigan: “If We Don’t Have That Cost-Sharing (Subsidy), We Have To Make Up The Difference And The Only Way For Us To Do That Is With A Higher Rate.” [Detroit Free Press, 6/14/17]

Dr. Mario Molina, Former CEO, Molina Healthcare: “The Administration And Republicans In Congress Want You To Believe That Insurers Raising Premiums For Their Plans Or Exiting The Marketplaces All Together Are Consequences Of The Design Of The Affordable Care Act Instead Of The Direct Results Of Their Own Actions To Sabotage The Law. Don’t Let Them Fool You.” [U.S. News & World Report, 5/30/17]

Brad Wilson, CEO, Blue Cross Blue Shield Of NorthCarolina: “The Failure Of The Administration And The House To Bring Certainty And Clarity By Funding CSRs Has Caused Our Company To File A 22.9 Percent Premium Increase, Rather Than One That Is Materially Lower.” [Washington Post, 5/26/17]

Kurt Giesa, Practice Leader, Oliver Wyman Actuarial Consulting: “Our Modeling Shows That This Uncertainty, If It Remains, Could Lead Payers To Submit Rate Increases Between 28 And 40 Percent, And More Than Two-thirds Of Those Increases Will Be Related To The Uncertainty Around CSR Payments And Individual Mandate.”[Oliver Wyman, 6/14/17]

Based on what we know so far, the reviews of Trump’s health care sabotage Executive Order aren’t pretty.

In fact, they’re downright scary.

President Trump’s pledge to sign an Executive Order later this week will sabotage health care, achieving his dream of health care repeal that failed with bipartisan opposition in Congress and overwhelming opposition from the American people.

Trump has been rooting for health care to fail, saying “Let it be a disaster,” and his sabotage will end protections for those with pre-existing conditions, raise health care premiums and deny access to coverage for millions of Americans — and could result in the collapse of the individual insurance market.

But don’t take our word for it.

Look at the early reviews that have exposed the truth…

Larry Levitt, Kaiser Family Foundation: “If the executive order is as expansive as it sounds, it could severely destabilize the individual and small business insurance markets. Association plans exempt from the ACA can cherry pick healthy people and make coverage unaffordable for those with pre-existing conditions. If loosely regulated association plans are allowed, insurers will leave the ACA marketplaces as soon as they can or hike premiums a lot.”

Larry Levitt, Kaiser Family Foundation: “The executive order also reportedly envisions expanding the use of short-term health insurance plans. Short-term insurance plans can offer inexpensive coverage to currently healthy people, but they exclude people with pre-existing conditions. If healthy people can enroll in short-term plans and avoid the individual mandate penalty, the ACA marketplaces could collapse. Anything that creates a parallel insurance market for healthy people will lead to unaffordable coverage for sick people. Middle class people with pre-existing conditions ineligible for ACA subsidies could be especially vulnerable under the executive order. You can bet this executive order will get challenged in court, but it could also create lots of confusion going into open enrollment.”

Cori Uccello, American Academy of Actuaries: “Cori Uccello, senior health fellow at the American Academy of Actuaries, said that one aspect to watch in the order is when the changes will take effect. Insurers have already set their prices and made plans for 2018. ‘Anything that applied to 2018 would be incredibly destabilizing,’ she said. ‘It would still be destabilizing in 2019 but people would know ahead of time.’”

Matt Fiedler, Brookings Institute: “‘Associations would siphon many healthier people out of the ACA-compliant market, driving up premiums,’ said Matt Fiedler, a fellow with the Center for Health Policy at Brookings Institute. ‘Higher premiums in the ACA-compliant market would result in big cost increases for many sicker enrollees — since they would not have the option of switching to the association market — and likely for the federal government as well.’”

Joseph Antos, American Enterprise Institute: “Joseph Antos, a health policy scholar at the conservative American Enterprise Institute, agrees. ‘Trying to exempt these new associations from ACA rules that apply to all other plans doesn’t strike me as something that’s going to stand up in federal court,’ Antos says.”

National Association of Insurance Commissioners: “AHPs would fragment and destabilize the small group market, resulting in higher premiums for many small businesses. … AHPs would be exempt from state solvency requirements, patient protections, and oversight exposing consumers to significant harm.”

Commonwealth Fund: “If they do so, the health insurance sold via the AHP could become exempt from consumer protections such as the essential health benefits standard and the prohibition on charging higher premiums to people with preexisting conditions. The result would be increased risk for higher premiums and fewer plan options on the individual market, as well as fraud and insolvency.”

Craig Garthwaite, Northwestern University: “‘There’s a general belief that at every turn the federal government is going to create regulations to hurt rather than help the markets,’ said Craig Garthwaite, director of the health care program at Northwestern University’s Kellogg School of Management, referring to the Trump administration. ‘It unwinds the ability of people with pre-existing conditions to get insurance under the ACA,’ Garthwaite said.”

Gary Claxton, Kaiser Family Foundation: “‘If the market’s already fragile right now, this is going to make it much more fragile,’ said Gary Claxton, director of the health-care marketplace project at the Kaiser Family Foundation. ‘All of this would be the start of the end of the individual ACA market.’”

Linda Blumberg, Urban Institute: “‘The risks of trying to do the kinds of things we’re hearing about are really tremendous,’ said Linda Blumberg, senior fellow at the Health Policy Center at the Urban Institute.”

Associated Press: “Without those healthy customers, the cost might rise faster for people with medical conditions.”

The Hill: “President Trump’s planned executive order on ObamaCare is worrying supporters of the law and insurers, who fear it could undermine the stability of ObamaCare.”

Washington Post: “If at first you don’t succeed at repealing Obamacare, try, try again — with an executive order. President Trump, desperate for a health-care win that Congress couldn’t hand him, is pursuing a backdoor way of letting more Americans buy insurance plans free of the Obamacare regulations that Republicans have blamed for big premium hikes and costly deductibles.”

Washington Examiner: “Both association health plans and short-term plans are less expensive than Obamacare plans because they offer limited coverage. They don’t guarantee same-cost coverage, or any coverage, for people with pre-existing illnesses and they do not cover a broad range of medical care, from addiction treatment to maternity care.”

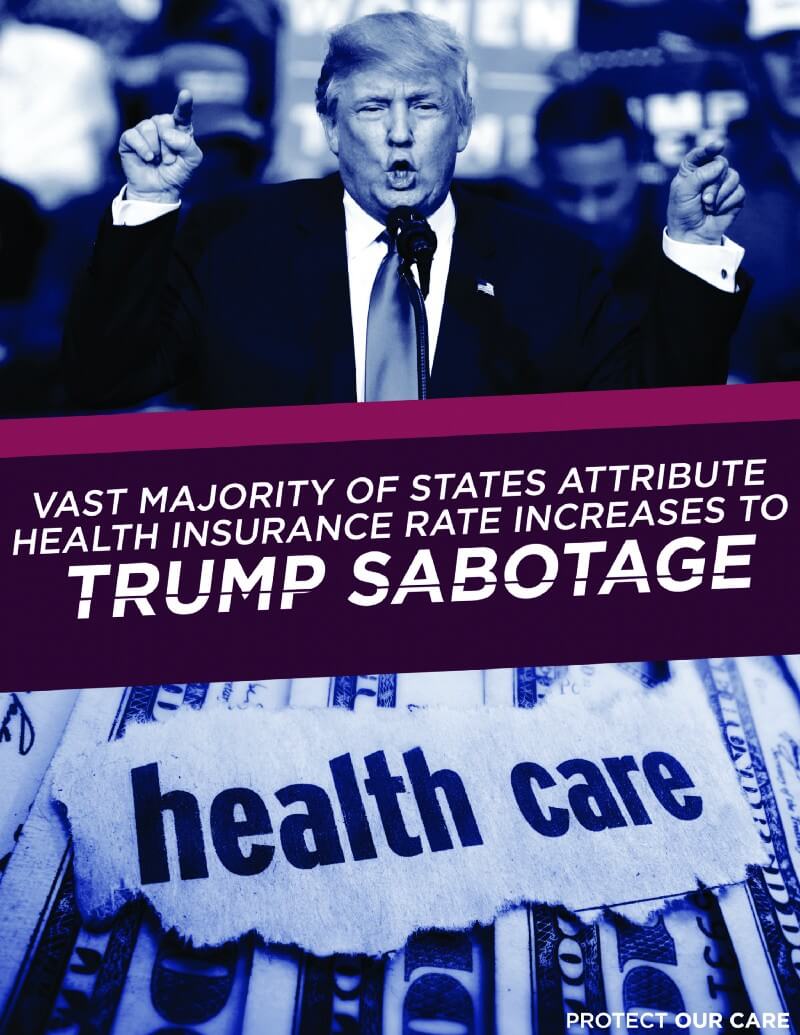

NEW REPORT: VAST MAJORITY OF STATES ATTRIBUTE HEALTH INSURANCE RATE INCREASES TO TRUMP SABOTAGE

The deadline for states to finalize premium rates for the individual and small group market and submit them to the federal government for approval was one week ago (9/27/17) and many states have publicly announced double-digit increases.

In a comprehensive review of all the 28 states whose final state-approved rates that have been made public, this new report from Protect Our Care shows that the vast majority — 20 states — attribute their rate increases in part to the Trump administration’s sabotage of our health care. Blame for the increase was squarely placed on the Trump administration and Republicans in Congress injecting uncertainty into the marketplace by threatening to default on cost-sharing reduction (CSR) payments that help lower out-of-pocket costs in some way, shape or form.

Our analysis finds:

20 states attribute rate increases to uncertainty over whether the Trump administration will make CSR payments: Connecticut, Florida, Georgia, Idaho, Illinois, Indiana, Louisiana, Maine, Michigan, Mississippi, New Mexico, New York, Ohio, Oregon, South Carolina, South Dakota, Tennessee, Utah, Virginia and Washington. (Oregon cited weakening enforcement of the individual mandate for some of its rate increase.)

Five states indicated their state increases would be even higher if they assumed the Trump administration would not be making the CSR payments: Arizona, Arkansas, Colorado, Maryland and Vermont.

Two states — Alaska and Minnesota — have mostly cut their insurance rates next year after the federal government allowed them to start a new reinsurance program.

One state, Nevada, did not release any reason for their 2018 rates.

While they’re not included in this analysis of rates, the sabotage has had other consequences including insurers that decided not to participate in the marketplace next year, citing the uncertainty the Trump administration had created. Anthem in Maine announced it was exiting the marketplace at the last minute, as well as Medica in North Dakota, to name a couple of examples.

We now have the clearest evidence yet that the Trump administration’s sabotage of our health care system is leading to the higher insurance rates we are seeing for 2018.

Prior to the Trump administration, independent analyses show that the Affordable Care Act was working. Standard’s & Poor said it expected insurers’ performance in the marketplaces to be better in 2016 than in 2015, and 2017 would be better than 2016. The nonpartisan Congressional Budget Office said it anticipated “the market to be stable” under the ACA. The average premium after tax credits increased by $1 dollar, from $100 in 2016 to $101 in 2017.

Evidence is Clear: States Blame Uncertainty for Even Higher Rates

Associated Press: “Jeff Stelnik, the [BCBS of AZ]’s senior vice president of strategy, sales and marketing, told The Associated Press the change came because of improved profitability on current plans and an assumption that the federal government will continue funding a program reducing some customer costs. The decision comes despite worries from many insurers that the “cost sharing reductions” they are required to offer many lower-income customers won’t be funded by the Trump Administration. ‘There still continues to be uncertainty in the marketplace, we still continue to be concerned by that uncertainty,’ Stelnik said. But he said a deadline for finalizing premiums for 2018 and a better balance between premiums and claims ‘enabled us to be confident in the new pricing that we are putting in the marketplace.’”

[Note: Insurers updated their rate requests on August 21 that reflected higher rates assuming no CSR payments. The state-approved rates are more aligned with the earlier requests.]

Colorado Division of Insurance: “In Colorado, premiums for individual plans (not from an employer) will be increasing by an average of 26.7 percent…The premiums would be up to 14 percent higher if we used the non-CSR-funded premium requests.”

Connecticut Insurance Department: “The federal funding of the CSR payments for coverage year 2018 would have reduced the approved rate increases from 27.7% to 16.8% for [ConnectiCare Benefits Inc] and from 31.7% to 24.7% for Anthem.”

“As a result of the lack of clarity about future funding of CSRs and the need to make rate determinations for 2018, the Department asked exchange carriers to make a supplemental filing which assumed CSRs would not be paid. The supplemental rate increase for non-payment of the CSRs is 16.7 percent, this is applied only to the Silver exchange plans. The increase in rates for the Silver exchange plans will be mitigated for consumers receiving tax credits by the increase in the federal tax credits for 2018.”

Miami Herald: “Florida regulators said most of the average rate hike — 31 percentage points [of the 44.7 percent total] — came from standard plans sold on the ACA exchange at Healthcare.gov. Insurers raised rates for those plans due to the political uncertainty that has plagued the healthcare debate, specifically whether the Trump administration will stop paying subsidies that lower out-of-pocket costs for low-income Americans.”

Atlanta Journal-Constitution: “Every single one of the four companies offering policies on the exchange here plans to raise their rates by an average of more than 50 percent, if Washington does not give certainty on the subsidy funding.”

Idaho Statesman: “‘The rate increases, in particular on silver-level plans, are definitely greater than we would like,’ said Idaho Department of Insurance Director Dean Cameron. ‘There is legitimate uncertainty” regarding whether the government will continue to pay for certain subsidies for low-income users of the exchange….The rates that insurers are slated to charge for “silver” plans next year would be cut by more than 20 percent if subsidies are continued, according to the Idaho Department of Insurance. And that would affect how much actual help consumers would get to pay for those pricey “gold” plans.”

Illinois Department of Insurance: “‘DOI is committed to ensuring that consumers are prevented from incurring higher health insurance costs due to uncertainty in Washington,’ said DOI Director Jennifer Hammer. ‘Insurers have been advised to apply the CSR uncertainty cost, solely to silver plans.’ This change makes it important that consumers diligently shop for a plan this year. DOI reminds consumers that cost alone may not be the only factor to consider when selecting a plan. For example, consumers may want to also consider a plan’s provider network.”

ABC 6 News: “University of Indianapolis’ Director of Public Health programs, Heidi Hancher-Rauch, said ‘uncertainty’ is the reason for rising costs. ‘Insurance companies are left trying to figure out, OK, if we aren’t going to get that money from the government, how are we going to make up that difference,’ said Hancher-Rauch. Another uncertainty is whether the requirement for everyone to get insurance will be enforced. ‘We rely on those healthy people who are paying into the plans to do that cost sharing among all of us,’ said Hancher-Rauch. ‘We absolutely need those healthy people paying into the insurance to help offset some of those costs for the older and sicker individuals.’”

Greater Baton Rouge Business Report: “Both Vantage and Blue Cross announced earlier this summer they would raise rates by double digits for those who buy insurance through the ACA exchanges. Vantage raised such rates by upwards of 30%, while Blue Cross increased rates by 18.5%.

The companies said the major driver of the rate increase was uncertainty over cost-sharing reductions, which are designed to help insurance companies offer affordable coverage to low-income people. President Donald Trump’s administration has threatened to stop paying the subsidies. Vantage and Blue Cross also cited a lax enforcement of the individual mandate, the provision of the ACA that requires everybody have insurance.”

Maine Public Radio: “Maine’s Insurance Superintendent Eric Cioppa approved rate increases that range from 20 to 37 percent if the cost-sharing payments end.”

Maryland Insurance Administration: “The rates do not include any factor based upon the political uncertainty of future cost-sharing reduction payments.”

Michigan Department of Insurance and Financial Services: The size of the increases this year is partially due to the uncertainty as to whether the federal government will continue to fund Cost Sharing Reduction (CSR) payments. Under the Affordable Care Act (ACA), insurers on the Marketplace are required to provide financial assistance under plans covering individuals up to 250% of the federal poverty level and eligible American Indians. The CSR payments allow insurers to meet that legal obligation without increasing rates. The President has indicated he does not support these payments, and the federal government is currently making them on a month-to-month basis.

Wall Street Journal: “Mississippi’s insurance commissioner, Mike Chaney, said he is approving a 47.4% average premium increase for the state’s one ACA exchange insurer, which would have been around 17.9% if the cost-sharing payments were guaranteed. The insurer couldn’t bear the potential extra expense of funding the cost-sharing subsidies without the bigger premium bump, he said: ‘They can’t take that, they just can’t do it.’”

Albuquerque Journal: “The state’s top insurance regulator said the rate increases in 2018 are heavily influenced by uncertainty about whether the federal government will block or discontinue payments to insurers. President Donald Trump has repeatedly threatened to halt these reimbursements to insurance companies in his drive to dismantle the Affordable Care Act, as Obamacare is formally known.”

New York Times: “In New Mexico, the average rate increase for plans sold on the state marketplace is about 30 percent. ‘Half of that increase is due to the uncertainty in Washington and the inability to lead,’ said John G. Franchini, the state insurance regulator. The four insurers selling policies in the state marketplace are offering more types of plans.

ODI: “In addition, the average cost of coverage for individual plans sold on the federal exchange in 2018 will be 34 percent higher than the average cost of coverage in 2017. Approximately 11 percent of that increase is attributable to the assumption that insurers will not receive Cost Sharing Reduction (CSR) payments in 2018.”

Kaiser Foundation Health Plan of the Northwest — 14.8 %

Moda Health Plan — 4.7 %

PacificSource Health Plan — 2.8 %

Providence Health Plan — 10.8 %

Oregon Department of Consumer and Business Services: “Reasons for the rate changes include: The new Oregon Reinsurance Program. This program reduced individual market rates by 6 percent, and added a 1.5 percent increase to the small group market. Federal weakening of the individual mandate enforcement. This increased rates by 2.4 percent and 5.1 percent.”

Charlotte Observer: “A ‘cost sharing reduction’ subsidy reduces the amount that patients pay for deductibles and copays. About 20 percent of the 31 percent increase in premiums for S.C. residents is attributed to the uncertainty of funding for that subsidy, said S.C. Department of Insurance Commissioner Ray Farmer.”

Argus Leader: “But insurance executives said political efforts to reform healthcare created the uncertainty that drove prices up in the first place.

Assuming President Donald Trump doesn’t move to eliminate cost-sharing reductions, policyholders will see a 7.5 percent bump under Sanford and 17 percent under Avera, executives from each group confirmed.”

The Tennessean: “Uncertainty — wrought by the ongoing debate over Obamacare repeal-and-replace legislation and decisions by the White House and HHS officials — have clouded the premium request process, and led to higher requests. Cost-sharing reductions, a subsidy that offsets out-of-pocket costs for some shoppers, are divisive in Washington, D.C. There is no long-term commitment that CSRs will be paid to insurers, and the decision is being made monthly. BCBST attributes nearly all of its average 21 percent premium increase request to the unknowns of the upcoming year.”

TDCI Commissioner McPeak: “Instead, it appears more likely that Tennesseans must prepare themselves for a round of actuarially justified rates for 2018 that are far higher than could be necessary as a result of uncertainty in Washington. On behalf of Tennessee consumers, I continue to urge Congress to take action to stabilize insurance markets. The Department stands ready to take action to aid consumers should stabilization measures be enacted.”

Deseret News: “Just the general increase in medical trends that we’ve seen over the past decade — as the cost of services increase, premiums increase,” [Utah Insurance Department spokesman Steve] Gooch said. ‘There’s (also) an increase due to the uncertainty over whether the (cost-sharing payments) will be funded. So that causes some uncertainty in the risk profile, so that’s kind of built into those (new) rates.’”

Addison County Independent: “If the cost sharing reduction payments were not continued, BCBS [which has 87 percent of the market] estimates premiums would go up by an additional 1.5 to 2 percent.”

Richmond Times-Dispatch: “As many see their options for health plans dwindle down to one insurer, premiums are simultaneously set to rise by an average of 57.7 % next year in Virginia’s individual marketplace…‘The rate increases can be attributed to an unstable market, with too few healthy people signing up to balance out the number of sick people who enroll, and the uncertainty of cost-sharing reduction payments, which are meant to go to insurers to cover the cost of offering lower prices to poor members, but which the federal government has refused to guarantee.’”

Washington Health Benefit Exchange Board: “Rates for the health plans certified represent a 24 percent increase over those available through the Exchange for 2017 coverage…However, should the federal government stop funding CSRs at some point in 2018, the OIC has determined that they may legally adjust the original lower rate to the approved higher rates of silver plans in the Exchange.”

The newest round of polling data is out from multiple sources but it all confirms the same thing — voters reject partisan health care repeal and disapprove of the leadership of those who keep up the relentless push.

New Quinnipiac University polling data shows only 19% support the Graham-Cassidy-Heller health care repeal, while 59% disapprove.

Support for repeal falls to only 14% among independents and is only 24% with white non-college educated voters.

Only 11% approve of how Republicans in Congress are handling health care with an overwhelming 81% disapproving, including 86% disapproval with independents.

Only 10% believe their health insurance costs would go down under the plan, while most voters think it will go up (44%) or stay the same (30%)

⅔ (67%) of voters — as well as 63% of Republicans — approve of preventing health insurance companies from raising insurance rates for people with pre-existing conditions, a provision this repeal would take a way.

New national polling from FOX News shows a record-level of support for the Affordable Care Act with 51% saying they are glad it passed and 42% saying they wish it never had.

The poll showed voters prefer to make “minor changes to Obamacare while largely leaving the law in place” by a 33 point margin (63% to 30%).

Only 25% supported the Senate’s health care plan — known as Graham Cassidy — in this poll while 51% oppose it.

New data from Public Policy Polling confirms the trend with voters preferring the Affordable Care Act over Graham-Cassidy-Heller by 19 points (53% to 34%).

Only 27% support for the latest GOP health care repeal bill with 53% opposed.

Only 32% think the best path forward is repeal, while 62% prefer we keep what works and fix what doesn’t.

This week witnessed the defeat of the fifth Republican health care repeal attempt, the Graham-Cassidy-Heller-Johnson bill. Every attempt to repeal the Affordable Care Act (ACA) raised premiums and costs, increased the number of people without coverage, allowed insurance companies to gut protections for people with pre-existing conditions, imposed an age tax on older Americans, and ended Medicaid as we know it.

At the same time Republicans threaten to try repeal again in 2018 — despite the public’s repeated rejection of their partisan efforts — the Trump administration and Republicans in Congress are doing everything they can to sabotage our current system.

This memo exposes those sabotage efforts, outlines how this sabotage is already raising people’s costs, and shows how the American people will hold Republicans accountable for their actions.

Republicans are Taking Deliberate Actions to Sabotage Our Health Care

These statements are false for two reasons. First, independent analyses show that the Affordable Care Act is working. Standard’s & Poor said it expected insurers’ performance in the marketplaces to be better in 2016 than in 2015, and 2017 would be better than 2016. The nonpartisan Congressional Budget Office said it anticipated “the market to be stable” under the ACA. The average premium after tax credits increased by $1 dollar, from $100 in 2016 to $101 in 2017. Currently, 10.2 million people are signed up for coverage in the marketplaces.

Second, the President’s statements do not accurately reflect reality. Republicans are not “letting” the ACA fail, as though they were just mere onlookers watching it happen. No. They are taking deliberate actions to sabotage the health care system. For example, on day one, the Trump Administration issued an executive order demanding federal agencies begin dismantling the Affordable Care Act without protecting parts that are working and without regard to the damage it would cause. Whatever President Trump’s motivation — personal hostility toward President Obama or simply spitefulness — the result is clear: his administration is making it harder for people to sign up for coverage and taking steps that are raising people’s premiums and destabilizing the marketplace.

Making it Harder for People to Enroll — Meaning Fewer Will Sign Up

The Trump administration is making it much harder for people to enroll in the marketplaces. For the final days of open enrollment in January 2017, the Trump Administration cut 75% of television advertising and all digital advertising that helped people find out about their health care options- resulting in an estimated 500,000 fewer people getting coverage.

Then, the Trump administration announced it was cutting the number of days people could sign up for coverage in half for future enrollment periods, from 90 days to 45 days.

For the open enrollment period that begins on November 1, 2017, the Trump administration already said it was cutting the outreach ad budget by 90 percent, from $100 million to just $10 million. The administration will be shutting Healthcare.gov down for part of the day on most Sundays. Sens. Brian Schatz (D-HI), Elizabeth Warren (D-MA), Cory Booker (D-NJ) and Chris Murphy (D-CT) wrote to the Department of Health and Human Services demanding answers about why this is going to happen.

This week, BuzzFeed News reported that the Trump administration ordered the Department of Health and Human Services’ regional directors to stop participating in open enrollment events. Mississippi Health Advocacy Program Executive Director Roy Mitchell said, “I didn’t call it sabotage…But that’s what it is.”

Add to that cuts to in person assistance, call centers being closed and a new final deadline to sign up.

All of these actions will result in reducing the number of people who sign up in the marketplaces. What this will mean is that those people who do sign up are more likely to be sicker and older, since they have a higher incentive to sign up than younger, healthier people. That in turn will cause premiums to spike. In other words, the Trump administration’s direct actions will be responsible for fewer people signing up for health care and raising premiums for those who do — a clear case of sabotage if there ever was one.

CSRs: Raising Rates and Destabilizing the Marketplace

Another big part of Trump’s sabotage campaign is his repeated threats to stop funding the cost sharing reductions (CSRs), which lower people’s out of pocket costs. The result: an increase in deductibles and out-of-pocket costs for the majority of those covered through the ACA marketplaces. As Sen. Lamar Alexander (R-TN) said, “Without payment of these cost-sharing reductions, Americans will be hurt.”

The proof is in the pudding. States that have finalized their rates for 2018 say they raised them even more because of the uncertainty over whether the Trump administration will pay these cost-sharing reductions. Experts agree, failing to make these payments will mean higher premiums and will explode the national debt.

Studies

Congressional Budget Office: Congressional Budget Office says that failure to make these payments would mean people’s health insurance premiums will go up 20 to 25 percent and add nearly $200 billion to the debt over the next decade.

Center for American Progress: “The Center for American Progress estimates that uncertainty around CSRs and mandate enforcement will raise 2018 premiums for benchmark coverage an extra $1,061 annually for a 40-year-old and $2,491 annually for a 64-year-old.”

Kaiser Family Foundation: “Benchmark premiums would increase by 19 percent on average if cost-sharing subsidies were unpaid.”

Urban Institute: “We find that premiums for silver marketplace plans would increase $1,040 per person on average.”

Urban Institute: “A precipitous drop in insurer participation is even more likely if the cost-sharing assistance is discontinued.”

Commonwealth Fund: “Eliminating cost-sharing reductions could destabilize insurance markets.”

Kurt Giesa, Practice Leader, Oliver Wyman Actuarial Consulting: “Our modeling shows that this uncertainty, if it remains, could lead payers to submit rate increases between 28 and 40 percent, and more than two-thirds of those increases will be related to the uncertainty around CSR payments and individual mandate.”

Teresa Miller, Pennsylvania Insurance Commissioner:“Failing to make payments to insurers for cost-sharing reductions would force insurers to request a statewide average 20.3 percent increase rather than 8.8 percent statewide average that was filed with the department in may.”

Mike Kreidler, Washington State Insurance Commissioner:“The current federal administration’s actions — such as not committing to reimburse insurers for cost-sharing subsidies and not enforcing the individual mandate — appear focused only on destabilizing the insurance market.”

Dave Jones, California State Insurance Commissioner: “President Trump appears on a mission to destroy health-insurance markets by creating instability through his own actions and thereby depriving millions of Americans of health-care coverage.”

Determination by the Florida Office of Insurance Regulation: “Florida regulators said most of the average rate hike — 31 percentage points [of the 44.7 percent total] — came from standard plans sold on the ACA exchange at Healthcare.gov. Insurers raised rates for those plans due to the political uncertainty that has plagued the healthcare debate, specifically whether the Trump administration will stop paying subsidies that lower out-of-pocket costs for low-income Americans.”

National Academy for State Health Policy: “The Federal Government must commit to funding CSR payments in order to lower rates and stabilize carrier participation.”

Dan Hilferty, President and CEO, Independence Blue Cross: “We firmly believe your coverage will be there for 2018, if the federal government, Congress and president commit to, fund the subsidies during an interim period of time.”

Dr. Mario Molina, Former CEO, Molina Healthcare: “The Administration and Republicans in Congress want you to believe that insurers raising premiums for their plans or exiting the marketplaces all together are consequences of the design of the Affordable Care Act instead of the direct results of their own actions to sabotage the law. Don’t let them fool you.”

Brad Wilson, CEO, Blue Cross Blue Shield of North Carolina: “The failure of the Administration and the House to bring certainty and clarity by funding CSRs has caused our company to file a 22.9 percent premium increase, rather than one that is materially lower.”

Americans Will Rightly Hold Republicans Accountable for Sabotage

President Trump and Republicans in Congress might hope that people will blame President Obama and Democrats for rising premiums and limited choices on the marketplace, but that is not the case. As the Wall Street Journal editorial board wrote, “Republicans run the government and that means they are responsible for what happens in health care.”

An April 2017 Kaiser Health tracking poll found that 64 percent of Americans, including ⅔ of independents and a majority of Republicans, said they would blame Republicans and President Trump for any future problems with health care and the Affordable Care Act (ACA) going forward. The same poll found that 74 percent want Trump and his Administration to do what they can to make the current law work — that includes 8 in 10 independents and over half of Republicans.

Moreover, a recent poll by Hart Research Associates found that “nearly two-thirds (64%) of voters believe it is true that Donald Trump is ‘undermining the Affordable Care Act’ and three-in-five (61%) voters believe that he is actively ‘trying to make the Affordable Care Act fail.’ Additionally, 64% say that Trump is ‘playing politics with people’s healthcare,’ including one-in-four (24%) of his own voters. Along similar lines, a 57% majority believe that the president is ‘sacrificing people’s health care in order to oppose Barack Obama.’”

Clearly, they are not fooling anybody. Take a look at some of the headlines this week after state’s announced their finalized insurance rates for next year:

Bloomberg: Obamacare Rates Rise in Markets Unsettled by Trump

USA Today: Obamacare rates soar as White House refuses to make long term commitment to subsidies

NBC News: Obamacare Repeal Failed, but the Damage Is Already Done

Stand Up to Sabotage

All of us need to play a role in standing up to the Trump administration and Republicans in Congress sabotaging our health care. Here are a few ways:

Demand Bipartisan Talks and Action to Stabilize the Health Care Market: Republicans and President Trump have injected uncertainty into the health care market by pursuing secretive, partisan repeal and by refusing to commit to paying CSRs. A bipartisan deal to pay CSRs was nearly in place until Republican leaders and President Trump pulled the plug so they could again try to ram through partisan repeal in the form of Graham-Cassidy. It’s now on Republicans to return to the table and pass a stabilization bill immediately; unfortunately, a lot of the damage has already been done and they will hold the bag for higher premiums, lost coverage and higher debt.

Demand Republicans Stand Up to Trump’s Sabotage of Open Enrollment and Shine a Light on What It Means: Republicans need to stand up to and speak out against the Administration’s effort to sabotage open enrollment and do their part to help get their constituents enrolled. Everyone must continue to shine a spotlight on every action (or inaction) along the way of the Trump Administration which undermines Open Enrollment through rapid response press, events in states, online activism and paid advertising so that we can hold people accountable.

Hold Republicans Accountable: We should let lawmakers know that if they are not going to stand up to the Trump administration’s sabotage, they are complicit in it. We should be making our voices heard at town hall meetings and calls to our Representatives. We need to expose these sabotage efforts, demand answers and use every tool at our disposal, protests, ads and other forms of activism to hold Republican lawmakers accountable for participating in or turning a blind eye to sabotage.

Today, the day of the only scheduled hearing on the GOP’s newest secret, partisan repeal bill, Senators Lindsey Graham (R-SC) and Bill Cassidy (R-LA) released yet another version of their bill. Like previous iterations, this bill would raise costs, lower options and end Medicaid as we know it — and go even further removing protections for people with pre-existing conditions. If Sens. Graham and Cassidy thought releasing a new version of their bill would make it better, they were highly mistaken. Take a look for yourself:

“The new version of Cassidy-Graham may be crueler and more cynical than the last.”

“[T]he new version appears to go further in weakening protections for sick people, apparently to win over conservatives who continue to express reservations, such as senators Rand Paul, Ted Cruz, and Mike Lee.”

“The bill continues, however, to give states broad new authority to allow insurance companies to provide skimpier plans with far fewer benefits while charging higher premiums to the sick and the old.” [

“States would have even more flexibility to roll back some of the Affordable Care Act’s insurance regulations — including the guarantees it provides for people with pre-existing conditions.”

Analysts Agree: Every State Loses Under Graham-Cassidy Affecting People’s Care. Multipleindependentanalyses — and even Trump’s own CMS — agree that states would be worse off if theGraham-Cassidy repeal bill passess. Over time, every state loses because Graham-Cassidy zeroes out its block grants and ratchets down its spending on the Medicaid per capita cap. This means people would not have access to the financial assistance to help lower their health care bills, and federal Medicaid funding would no longer adjust for public health emergencies, prescription drug or other cost spikes, or other unexpected increases in need.

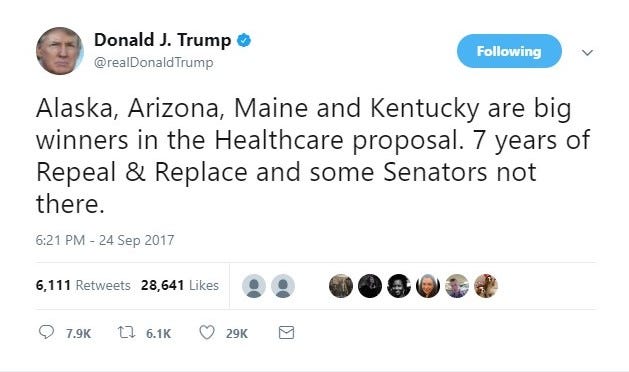

Alaska stands to lose $2 billion from 2020–2027 and $14 billion over the next two decades.

Arizona stands to lose $19 billion from 2020–2027 and $133 billion over the next two decades.

Maine stands to lose $2 billion from 2020–2027 and $17 billion over the next two decades.

Kentucky stands to lose $11 billion from 2020–2027 and $81 billion over the next two decades.

And according to an AARP analysis, the bill’s age tax would lead to huge increases in total costs for a 60-year-old making $25,000 in each of these states:

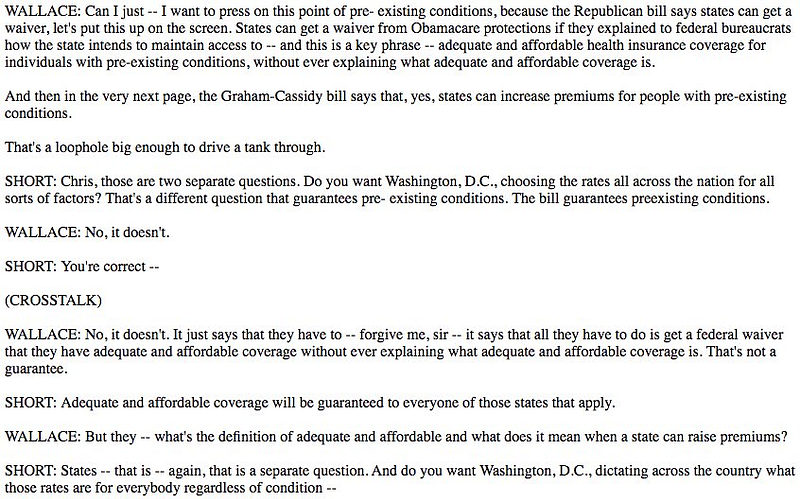

On Fox News Sunday this morning, White House legislative affairs director Marc Short admitted that the Graham-Cassidy health care repeal bill eliminates protections for people with pre-existing conditions.

Since the Affordable Care Act was passed, the most popular and essential provisions in the law has been coverage for pre-existing conditions. As many as half of all Americans have them, and Republicans have consistently paid lip service to continuing to ensure they will be covered. The GOP’s latest repeal bill, however, allows states to waive these protections — paving the way for insurance companies to once again discriminate against hundreds of millions of people. And as the bill heats up, so has the coverage highlighting the GOP’s plan…

Associated Press: Winners and losers in GOP’s last-ditch health overhaul

“Losers — People with health problems or with pre-existing medical conditions could be charged more if the state they live in obtains a waiver from current requirements that forbid insurers from charging higher premiums based on health status. States could also seek waivers from the current requirement that insurers cover 10 basic kinds of services, such as maternity and childbirth, or mental health and substance abuse treatment.”

The Hill: GOP takes heavy fire over pre-existing conditions

“The new ObamaCare repeal measure from Senate Republicans would give states a way to repeal protections for people with pre-existing conditions, a controversial move that opponents of the bill are denouncing.”

Vox: How Cassidy-Graham brings back preexisting conditions

“The new Republican plan to repeal Obamacare would bring preexisting conditions back to the individual market, allowing insurers to charge sick people higher premiums — or deny them coverage outright. ‘You can be charged more for a specific condition,’ says Chris Sloan, a senior manager at the health research firm Avalere, of the Cassidy-Graham plan that has begun to gain traction on Capitol Hill.”

Bloomberg: GOP Health Bill Would End Guarantee That Sick People Won’t Pay More

“Under the latest Republican bill, states could get a waiver allowing insurers to charge people more if they or a dependent have a pre-existing condition, or if they get sick and want to keep their insurance. The key provision in the bill has vague language requiring a state to first show how it ‘intends to maintain access to adequate and affordable health insurance coverage for individuals with pre-existing conditions.’”

Politico: Kimmel, not Cassidy, is right on health care, analysts say

“But experts say that Cassidy and Graham’s bill can’t guarantee those protections and that Kimmel’s assessment was basically accurate because of the flexibility the bill gives states to set up their own health care systems. For example, health insurers could hike premiums for patients with pre-existing conditions if their states obtain waivers from Obamacare regulations — as Kimmel said.

NPR: Latest GOP Effort To Replace Obamacare Could End Health Care For Millions

“But many experts say the bill would have an impact similar to earlier Republican proposals for repealing the Affordable Care Act. Graham-Cassidy would eliminate coverage for many low-income people who gained insurance through the Medicaid expansion and could gut protections for people with existing medical conditions because states would be encouraged to seek waivers from the federal government’s rules on what must be covered.

The Hill: Blue Cross warns GOP repeal bill ‘undermines’ pre-existing condition rules

“The Blue Cross Blue Shield Association warned against a new GOP ObamaCare bill on Wednesday, saying it would ‘undermine’ protections for pre-existing conditions. ‘The bill contains provisions that would allow states to waive key consumer protections, as well as undermine safeguards for those with pre-existing medical conditions,’ the association said in a statement.”

NBC News: New GOP Plan Could Sow Health Care Chaos

“Most notably, states could free up insurers to charge people more for pre-existing conditions or reduce their plan’s benefits, which could open up customers to annual or lifetime caps on coverage.”

New York Magazine: 4 Ways Graham-Cassidy Would Make the Health-Care System Far Worse

“Under Graham-Cassidy, insurers could not refuse to cover someone because of a preexisting condition, but they would be able to make coverage so exorbitantly expensive that sick people couldn’t afford it.”

The reviews are in for Graham-Cassidy, the latest iteration of the GOP’s secret, partisan health care bill which would raise costs, lower choices, eliminate protections for pre-existing protections and gut Medicaid. There is perhaps no state which would fare worse than Alaska, which could see a 65% percent reduction in federal funding and cost increases to the tune of $31,790 more per year in premiums and out of pocket costs for a 60-year old making $25,000 per year starting in 2020. Alaska Governor Bill Walker said yesterday, “Alaska would fare very, very poorly. Nothing has been brought to my attention that would increase my comfort level.”

Just take a look at the headlines…

Alaska Dispatch News: State analysis predicts a rough road for Alaska under GOP health care legislation

The Midnight Sun: Alaska would lose 38 percent of federal health care funding under Graham-Cassidy

Fairbanks Daily News-Miner: Medicaid directors, including Alaska’s, sign statement critical of GOP health bill

NBC KTVU 2: Alaska DHSS releases preliminary analysis into Graham-Cassidy’s impact on Alaska

State of Reform: Alaska Commission on Aging comments on Graham-Cassidy

Daily News Miner: Studies: GOP health care proposal could prove costly for Alaskans

KTVA: Mother: Healthcare repeal could mean ‘difference between life and death’

Daily News Miner: Walker airs concern about latest GOP health care bill

Contact Our Press Team

For all press inquiries or if you would like to be added to our press list, please contact our press office at [email protected].