Not Only Would 20+ Million Lose Coverage, but the Entire Health Care System Would Be Thrown Into Chaos

Over the weekend, Governor Ron DeSantis (R-FL), Senator Lindsey Graham (R-SC), former Governor Nikki Haley (R-SC), and leading GOP Senate candidate Tim Sheehy (MT) echoed Donald Trump’s latest calls to “terminate” the Affordable Care Act (ACA). The MAGA GOP refuse to give up their war on health care, despite the ACA being more popular than ever with a record number of signups.

The consequences of ACA repeal would touch nearly every household in the country: in addition to 20 million losing coverage, over 135 million Americans with pre-existing conditions would lose critical protections, 49 million seniors would have to pay more for prescription drugs, and insurance companies would not be required to cover preventative care, such as vaccinations, contraception, and cancer screenings, and once again impose annual and lifetime limits on benefits and charge women more.

Thirteen years after it was signed into law, the ACA is now woven into the fabric of our lives. Millions of Americans depend on the ACA in order to stay healthy. At a time when more people are covered by the ACA than ever before, the consequences would be devastating, particularly for women, people of color, older adults, people who live in rural areas, people with disabilities, and the LGBTQI+ community.

If the Affordable Care Act is repealed:

- GONE: 2.3 million adult children will no longer be able to stay on their parents’ insurance.

- GONE: Insurance companies will be able to charge women more than men.

- GONE: Ban on insurance companies having annual and lifetime caps on coverage.

- GONE: Requirements that insurance companies cover prescription drugs and maternity care.

- GONE: Protections for 135 million Americans with pre-existing conditions, including 54 million people with a pre-existing condition that would make them completely uninsurable.

- GONE: Medicaid expansion, which covers more than 22 million people.

- GONE: Quality, affordable coverage that over 15.5 million people who buy insurance on their own.

- GONE: Premium tax credits that make premiums affordable for 80 percent of people who purchase health care on the marketplace.

- GONE: 49 million seniors will have to pay more for prescription drugs because the Medicare ‘donut hole’ will be reopened.

- GONE: Critical funding for rural hospitals.

- GONE: 61.5 million Medicare beneficiaries will face higher costs and disruptions to their medical care.

Republican Threats Could Lead To Nearly 40 Million People Losing Their Coverage

- 40 Million People Would Lose Coverage. If Republicans succeed in repealing the ACA, nearly 40 million people will lose coverage. In 2023, over 16 million people have signed up for ACA marketplace coverage, over 22 million people are enrolled in Medicaid expansion coverage available due to the ACA, and another 1 million people have coverage through the ACA’s Basic Health Program.

- The Uninsured Rate Would Increase By 69 Percent. Repealing the ACA would increase the number of uninsured Americans from 26.6 million to 61.6 million, according to 2020 data. Americans of all ages would be impacted by coverage losses:

- 1.7 million children would become uninsured, an increase of 48 percent.

- 4.9 million young adults aged 19 to 26 would become uninsured, an increase of 76 percent.

- 8.8 million adults aged 27 to 49 would become uninsured, an increase of 60 percent.

- 5.6 million million older adults aged 50 to 64 would become uninsured, an increase of 95 percent.

Overturning The ACA Would Worsen Racial Disparities In Health

The uninsured rate for Black Americans would spike to 20 percent, 32 percent for American Indian/Alaska Natives, 17 percent for Asian/Pacific Islanders, and 33 percent for Hispanics — compared to 13 percent for white Americans.

- 3.1 Million Black Americans Would Lose Coverage. The Urban Institute estimates that 3.1 million Black Americans would become uninsured if the ACA were overturned. According to the Center on Budget and Policy Priorities, the ACA helped lower the uninsured rate for nonelderly African Americans by more than one-third between 2013 and 2016 from 18.9 percent to 11.7 percent.

- 5.4 Million Latinos Would Lose Coverage. The percentage of people gaining health insurance under the ACA was higher for Latinos than for any other racial or ethnic group in the country. According to a study from Families USA, 5.4 million Latinos would lose coverage if Republicans repeal the ACA.

- 1.3 Million Asian/Pacific Islanders Would Lose Coverage. 1.3 million Asian/Pacific islanders would become uninsured if the ACA were overturned, according to estimates from the Urban Institute. Research shows the ACA cut uninsurance rates among Asian Americans by more than half–from nearly 20 percent to just under 8 percent — eliminating coverage disparities with white Americans.

- 488,000 American Indians And Alaska Natives Would Lose Coverage. According to the Urban Institute, the uninsurance rate for American Indians and Alaska Natives would more than double in 10 states if the ACA is overturned. Nationwide, 488,000 would lose coverage.

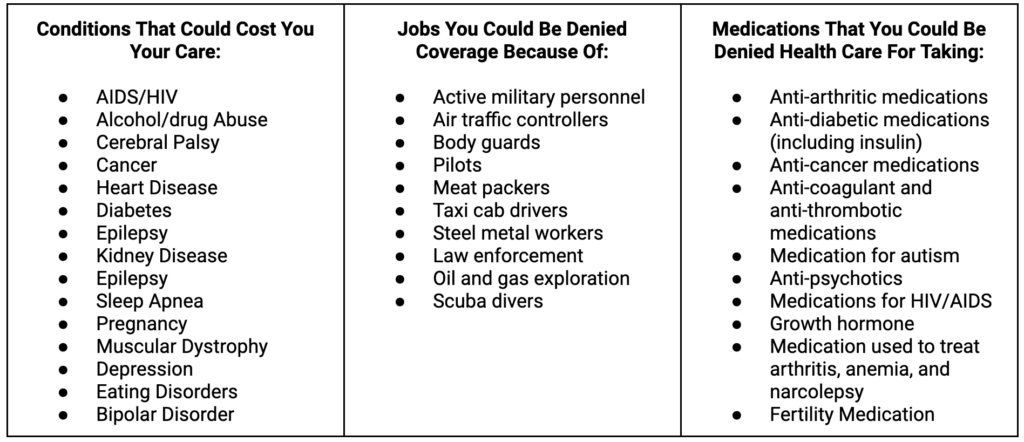

Republicans Want To Put Insurance Companies Back In Charge, Ending Protections For The 135 Million People With A Pre-Existing Condition

- According to a recent analysis by the Center for American Progress, roughly half of nonelderly Americans, or as many as 135 million people, have a pre-existing condition. This includes:

- 44 million people who have high blood pressure

- 45 million people who have behavioral health disorders

- 44 million people who have high cholesterol

- 34 million people who have asthma and chronic lung disease

- 34 million people who have osteoarthritis and other joint disorders

- More than 17 million children, 68 million women, and 32 million people aged 55-64 have a pre-existing condition.

Republicans Want To Give Insurance Companies The Power To Deny Or Drop Coverage Because Of A Pre-Existing Condition

Before the Affordable Care Act, insurance companies routinely denied people coverage because of a pre-existing condition or canceled coverage when a person got sick. Now insurance companies could have the license to do this again.

- A 2010 congressional report found that the top four health insurance companies denied coverage to one in seven consumers on the individual market over a three-year period.

- A 2009 congressional report found that some of the largest insurance companies had retroactively canceled coverage for 20,000 people over the previous five-year period.

- The Kaiser Family Foundation estimates that 54 million people, or 27% of adults aged 18 to 64, have a condition that would have been grounds for coverage denial in the pre-ACA marketplace.

Coronavirus Could Be Considered A Pre-Existing Condition. Without the ACA, millions of Americans who have contracted the coronavirus would likely be deemed as having a pre-existing condition and be at the mercy of their insurance companies who could refuse to pay for needed care.

Source: Kaiser Family Foundation, 2016; 2019

Source: Kaiser Family Foundation, 2016; 2019

Republicans Want To Give Insurance Companies The Power To Charge You More, While Their Profits Soar

- Premium Surcharges Could Once Again Be In The Six Figures. Republican threats to repeal the ACA could mean insurance companies once again could charge people more because of a pre-existing condition. The 2017 House-passed repeal bill had a similar provision, and an analysis by the Center for American Progress found that insurers could charge up to $4,270 more for asthma, $17,060 more for pregnancy, $26,180 more for rheumatoid arthritis and $140,510 more for metastatic cancer.

- Women Could Be Charged More Than Men For The Same Coverage. Prior to the ACA, women were often charged higher premiums on the nongroup market than men were charged for the same coverage.

- People Over The Age of 50 Would Face A $4,000 “Age Tax.” Without the ACA, insurance companies could charge people over 50 more than younger people. The Affordable Care Act limited the amount older people could be charged to three times more than younger people. If insurers were to charge five times more, as was proposed in the 2017 Republican repeal bill, that would add an average “age tax” of $4,124 for a 60-year-old in the individual market, according to AARP.

- 80 Percent of People With Marketplace Coverage Would Pay More. If the ACA is repealed, consumers would no longer have access to tax credits that help them pay their marketplace premiums, meaning 80 percent of people who have marketplace coverage would see price increases.

- Seniors Would Have To Pay More For Prescription Drugs. Republicans’ plan to repeal the ACA, would make 49 million seniors pay more for prescription drugs because the Medicare “donut” hole would be reopened.

- 60 Million Medicare Beneficiaries Could Face Higher Costs. In addition to paying more for preventive care and prescription drugs, Medicare beneficiaries could face higher premiums without the cost-saving measures implemented under the ACA. If Republicans are successful, seniors will also face less coordinated care.

- Insurance Companies Would Not Have To Provide The Coverage You Need. The Affordable Care Act made comprehensive coverage more available by requiring insurance companies to include “essential health benefits” in their plans, such as maternity care, hospitalization, substance abuse care, and prescription drug coverage. Before the ACA, people had to pay extra for separate coverage for these benefits. For example, in 2013, 75 percent of non-group plans did not cover maternity care, 45 percent did not cover substance abuse disorder services, and 38 percent did not cover mental health services. Six percent did not even cover generic drugs.

Republicans Want To Give Insurance Companies The Power To Limit The Care You Get, Even If You Have Insurance Through Your Employer

- Insurers Could Reinstate Lifetime And Annual Limits On 179 Million Privately Insured Americans. Repealing the Affordable Care Act means insurance companies would be able to impose annual and lifetime limits on coverage for those insured through their employer or on the individual market. In 2009, nearly 6 in 10 (59%) covered workers’ employer-sponsored health plans had a lifetime limit, according to the Kaiser Family Foundation.

- Americans Could Once Again Have To Pay For Preventive Care. Because of the ACA, health plans must cover preventive services — like flu shots, cancer screenings, contraception, and mammograms – at no cost to consumers.

- Employers Could Eliminate Out-Of-Pocket Caps, Forcing Employees To Pay More For Care. Under the ACA, health insurers and employer group plans must cap the amount enrollees pay for health care each year. If the law is overturned, these cost-sharing protections would be eliminated. The ACA also barred employer plans from imposing waiting periods for benefits that last longer than three months.

Republicans Want To End Medicaid Expansion

- More Than 21 Million People Enrolled Through Medicaid Expansion Would Lose Coverage. As of 2022, more than 21 million people were enrolled in Medicaid in over 40 states and territories.

- Access To Treatment Would Be In Jeopardy For 800,000 People With Opioid Use Disorder. Roughly four in 10, or 800,000 people with an opioid use disorder are enrolled in Medicaid. Many became eligible through Medicaid expansion.

- Key Support For Rural Hospitals Would Disappear. States that haven’t expanded Medicaid have poorer financial performance than states that have expanded Medicaid. If Medicaid provisions in the ACA were to be stripped, all rural hospitals would face this financial cliff.

Republicans Are Willing To Sacrifice Your Care For More Tax Cuts For The Wealthy

- The Richest Americans Would See Tax Cuts Averaging $200,000. Overturning the ACA would cut taxes for the top 0.1 percent of earners by an average of $198,000.

- Drug Companies Would Save Billions. If the ACA is struck down, pharmaceutical companies would pay $2.8 billion less in taxes each year.

- Repeal Would Weaken The Medicare Trust Fund. A significant portion of the tax cuts resulting from ACA repeal would come “at the direct expense of the Medicare Trust Fund,” according to the Center on Budget and Policy Priorities.